Fast facts on the temporary loss carry-back scheme

If you’re a New Zealand business that has been affected by the economic volatility which COVID-19 has brought, you may have already heard about the COVID19 temporary loss carry back scheme which the New Zealand government rolled out in the week beginning 27 April. This bill has been developed to take the financial strain off businesses who may have large amounts of tax to pay, but expect to, or are currently making a loss for the financial year ahead.

Keep reading to find out more about this bill, if your business may be eligible and how we can help you through this process. Plus we’ve included a handy infographic and example that helps explain the scheme.

What is the COVID-19 temporary loss carry back scheme?

Inland Revenue has developed a scheme which allows businesses that predict a loss in either the 2019/20 or 2020/21 financial year to estimate the loss for this year and neutralise profits from the previous year (i.e. carrying the loss back to the previous year). This means that they may refund some or all of the tax which the company paid in the previous profitable year, which allows extra cashflows for businesses currently under financial stress.

Is my business eligible?

If you have a business in New Zealand which made profit the year before and has or is expecting to make a loss the following year, your company may be able to apply for some or all tax expenses refunded.

If you think this sounds similar to your business, we can help you check other eligibility criteria below.

Other eligibility criteria:

- The company has maintained at least 49% common ownership in the year which proceeds a loss and the previous year

- The group has retained 66% common ownership in the year which proceeds a loss and the previous year

- The business has adequate imputation credit account balance to cover any refund

In other words, if your company has majority of its control and was financially sound, this new bill may apply to your business. These terms might seem like jargon to many, but don’t worry- it’s our job to help. We can take you through these steps to see if your eligible.

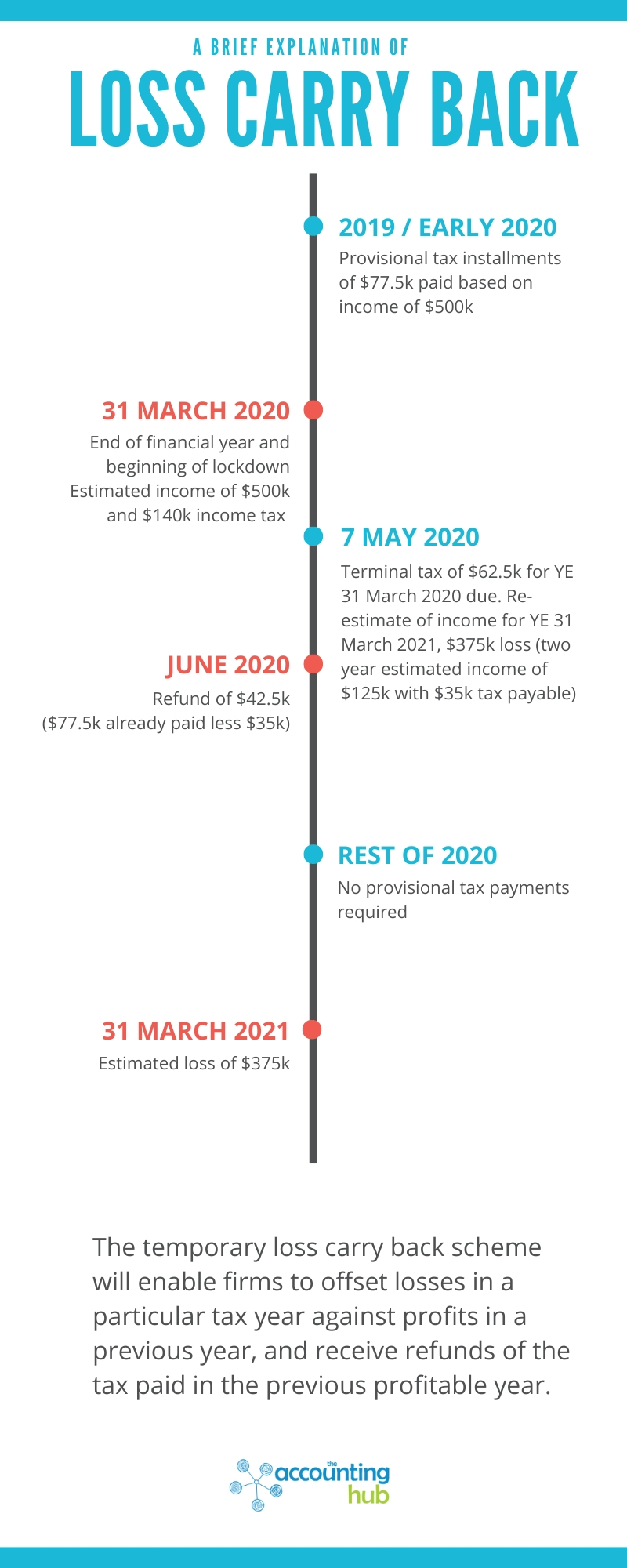

Example: The Blue Room Café & Bar

Before the effects of COVID-19 were felt, The Blue Room Café & Bar was having a profitable year for the financial period ended 31 March 2020. They have not yet finalised their tax return, but they are expected to return $500k net income. Their final provisional tax payment for the expected $500k income was due on May 7, where they were to pay $62.5k in tax (they have already paid $77.5k in early provisional tax instalments).

However, because of COVID-19, they haven’t been operating for the last few weeks, and they don’t not know when how busy it will be at level 2 and level 1. They’re still paying staff (supported by the wage subsidy scheme) and rent.

The owners sat down to do some forecasting and have estimated they will make a loss of the $375k loss in the year ended 31 March 2021, down from an estimated profit of $500k. Aggregating the two financial years 2020 and 2021, The Blue Room estimates an $125k of income with $35k tax payable. Because they’ve already paid $77.5k in tax, they pay nothing on May 7, and receive a refund of $42.5K from their earlier provisional tax payment.

How to claim the loss carry back

There are two different methods which we can help you with to claim your loss carry back. When you’re filing your tax returns for the financial year, we can help you include the carried-back loss. By using this method, IRD will automatically refund your overpaid tax. The second method is asking for a refund of provisional tax which your business has paid for the previous profitable year if you plan to carry back a loss from the 2021 financial year.

If this process seems a little out of your depth but you think you might be eligible, get in touch with us today to simplify your accounting processes. We can help you apply for the COVID-19 temporary loss carry back scheme and manage cashflows to get your business back on track.